GASB 84: Legal Considerations for Public Schools in Michigan

With the July 1, 2019 implementation date fast approaching for the new GASB 84[1] accounting guidance for fiduciary activities, school districts in Michigan have been working through various issues which have arisen in the implementation process. The new guidance will impact the accounting for many of the fiduciary/custodial activities currently reported by a school district in its Agency Fund. The most common of these activities are the various student- and school-related activity funds held in a bank account maintained by the school district. Examples of these activities include PTA/PTOs, boosters, class gifts, clubs and other student- and school-related activities. GASB 84 may also be applicable to funds held in a private purpose trust fund (e.g. a scholarship fund) where no formal trust has been established for the funds.

The objective of GASB 84 is to improve the guidance regarding the identification and reporting by state and local governments of their fiduciary activities. Under GASB 84, once a fiduciary activity is identified, it is required to be reported in one of four described fiduciary funds, only two of which (the private purpose trust fund and the custodial fund) are applicable to school districts. These fiduciary funds will be subject to the new accounting and reporting requirements under GASB 84.

If an activity is not identified as a fiduciary activity under GASB 84 (which in most instances will be due to the school district's level of administrative control over an activity's funds), it will be deemed a governmental activity and will be required to be reported in a governmental fund.

As part of the GASB 84 implementation process, the Michigan Public Schools Accounting Manual has recently been amended to comply with this new accounting guidance[2]. Under these changes, the prior "Agency Fund" has been replaced with the "Fiduciary Fund" for a school district's fiduciary activities (i.e. private purpose trust funds and custodial funds). Activities that are not identified as a fiduciary activity are required to be treated as governmental activities and included in either the General Fund or in a Special Revenue Fund (i.e., new Student/School Activity Fund (Fund Code 29)).

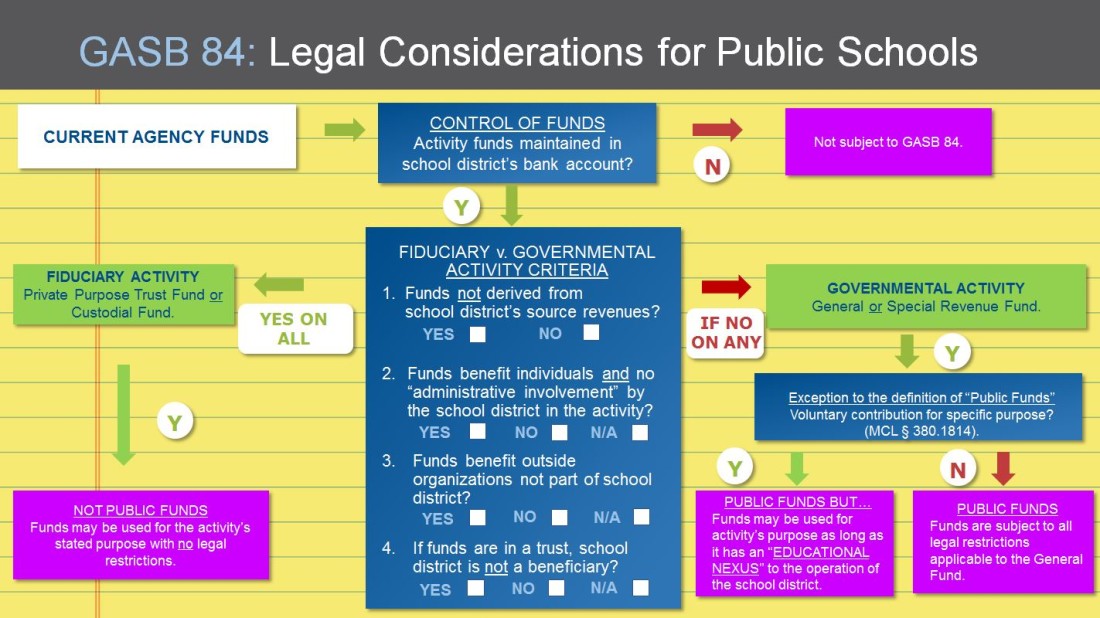

In addition to various accounting issues, GASB 84 has triggered several legal questions which we address in the next section. We have also prepared the following flow chart to assist school districts with the analysis of these legal issues.

LEGAL CONSIDERATIONS

Fiduciary v Governmental Activity

Under GASB 84, a "fiduciary activity" for a school district is identified based on various criteria which generally focus on the source of and the control over the activity's assets. GASB 84 provides the following criteria applicable to school districts for determining whether an activity is a fiduciary activity:

- The activity's assets must be controlled by the school district (e.g. school district's bank account or ability to direct use of funds);

- The activity's assets cannot be derived from the school district's source revenues (e.g. State Aid, property taxes, grants, fees, service revenues, sale of property, etc.);

- The activity's assets must be for the benefit of individuals and the school district and the school district does not have administrative involvement with the assets or the activity's assets must be for the benefit of organizations or other governments that are not part of the school district.

- If the assets are held in trust, the school district cannot be a beneficiary of the trust, the assets are dedicated to providing benefits to recipients in accordance with the terms of the trust and the assets are legally protected from the school district's creditors.

Of particular concern to school districts is the criterion which indicates an activity that benefits individuals will not be deemed a fiduciary activity if a school district has administrative involvement with an activity's assets. The GASB has developed examples and other literature to assist in applying the concept of "administrative involvement." Key examples of administrative involvement with the assets provided under GASB 84 include the following:

"a government has administrative involvement with the assets if, for example, it (a) monitors compliance with the requirements of the activity that are established by the government or by a resource provider that does not receive the direct benefits of the activity, (b) determines eligible expenditures that are established by the government or by a resource provider that does not receive the direct benefits of the activity, or (c) has the ability to exercise discretion over how assets are allocated."

In addition, GASB has released a draft of an Implementation Guide for GASB 84[3] which provides further guidance and examples on the determination of whether a government has administrative involvement over an activity’s assets. In this regard, the Implementation Guide provides in pertinent part as follows:

"In assessing whether a government has administrative involvement, a “substance versus form” consideration is appropriate. That is, the government’s role would have substance if the school board, school administrator, or faculty advisor (representative of the school establishes how the resources can be spent through approved policies."

The Implementation Guide also provides several examples with respect to student clubs which are not separate legal entities from the school district. A summary of these examples are as follows:

Q: A school board is responsible for establishing fees charged by student clubs?

A: Yes, administrative involvement by the school district.[4]

Q: The student club president, with the members of the club, establishes how resources can be spent and approves disbursements from the account?

A: No administrative involvement by school district.

Q: Parents of the club members establish how resources can be spent?

A: No administrative involvement by school district.

Q: Disbursements from the club are approved by a faculty advisor assigned to the club on behalf of the school district?

A: Yes, administrative involvement by the school district.

Q: School board establishes and approves policies related to the receipt, disbursement and holding of funds for student clubs?

A: Yes, administrative involvement by the school district.

Q: School board establishes and approves policies which only addresses issues such as authorized account signers and the prohibition of spending for illegal activities?

A: No administrative involvement by school district.

Q: State establishes specific guidelines on how club resources can be spent through administrative policy?

A: Yes, administrative involvement by the school district.

Over the years, many school districts have been adopting policies and guidelines providing various levels of oversight and control of funds for activities reported under its Agency Funds in an effort to safeguard these funds and to protect the school district from potential liability and negative exposure. Unfortunately, in many instances this oversight and control may now cause these activities to be deemed a governmental activity rather than a fiduciary activity under GASB 84. In practical terms, the fiduciary activity criteria focus on a key concept: who is calling the shots? As a result, after GASB 84 is implemented, many school districts will end up with custodial activities previously reported in an Agency Fund being treated as a governmental activity reported in the school district's General or Special Revenue Fund subject to the normal General Fund accounting and financial reporting rules.

From a legal standpoint, once in the General or Special Revenue Fund these funds will be deemed to be public school funds and accordingly, expenditures for an activity may be limited or restricted under state law and may also be subject to the procurement/purchasing requirements under state law and applicable board policies. Both of these issues are further discussed below.

In order to avoid activities being included in the General or Special Revenue Fund, a school district could choose to change the oversight or control it has over the activity so that it does not have administrative involvement over the activity. Alternatively, a school district could require that the activity be conducted through or by a separate entity outside of the school district. Typically this would be accomplished by having the group establish a separate legal entity such as a nonprofit corporation. It may also be possible for certain activities to be moved to existing organizations that are affiliated with the school district, such as an educational/booster foundation, PTA/PTO or a donor-advised fund established through a community foundation operating in the area.

Restrictions on Expenditures from a Fiduciary Fund?

Prior to GASB 84, fiduciary/custodial activities in an Agency Fund and private purpose trust funds were typically not treated as public school funds and accordingly were not subject to any restrictions on the expenditure of these funds under state law. We expect this will also be the case for fiduciary activities identified under GASB 84 and reported in a Fiduciary Fund. These funds will be treated as custodial in nature and will not be subject to any of the limitations or restrictions under state law applicable to a school district's public school funds held in its General or Special Revenue Fund.

Restrictions on Expenditures from the General or Special Revenue Fund?

The most significant legal concern arising with respect to the implementation of GASB 84 is the case where a previous fiduciary/custodial activity benefiting individuals is now deemed to be a governmental activity as a result of a school district's administrative involvement, and thus is required to be reported in the school district's General or Special Revenue Fund. The legal concern is whether the expenditure of these funds will now be limited or restricted to expenditures that a school district may legally make under state law from its public school funds.

For many school districts, the activities currently reported in an Agency Fund are for student activities, clubs, scholarship funds or booster groups with funds typically generated from donations, fees or other fundraising activities. The expenditures from these activities would presumably be to accomplish the group's stated purpose. These expenditures often include gifts, travel, mini-grant programs, materials, supplies and equipment, entry fees, scholarships, charitable contributions and other expenditures to carry out the group's stated purpose.

When determining whether an expenditure of public school funds is allowable, we typically utilize a two-step legal analysis. Under this analysis, we must first determine whether the school district is authorized to make the expenditure, and if it is authorized, the next step is to determine whether any specific limitation or restriction on the expenditure exists in contravention to this authority.

Under a Michigan school district’s general powers authority[5], an expenditure is generally allowable if it has a reasonable "educational nexus" to the operation of the school district in carrying out its educational mission, and there is no specific limitation or prohibition on the expenditure in contravention of this general powers authority. Funds held by a school district on a fiduciary/custodial basis for the typical student activity, club or booster group will typically be funds generated by donations, fees or other fundraising activities. The expenditures from these funds in most instances will have an educational nexus to the operation of the school in that the activity is for the benefit of students or the school.

The next question with respect to these funds would be to determine whether any specific limitations or restrictions might apply to the expenditure of these funds which might limit the school district's general powers authority. The Revised School Code and the State School Aid Act set forth various limitations and restrictions on the use of public school funds. Many of these limitations and restrictions are based on the source of the funds. For instance, there are specific limitations provided for the expenditure of State School Aid, operating taxes and voter authorized debt and sinking fund millages. In addition, the School Code provides certain prohibitions based on specific uses. For example, the School Code restricts or prohibits the expenditure of public school funds for cars, chauffeurs, mercury, performance enhancing drugs, alcohol, jewelry, gifts, golf, foreign goods and retroactive compensation.

A school district's custodial activity funds would rarely contain any of a school district's source revenues and thus would typically not be subject to any source limitations. The only other specific use restriction that might be applicable is the restrictions under Section 1814 of the Revised School Code (MCL §380.1814) which prohibits the use of public funds under the control of a school district for the purchase of alcoholic beverages, jewelry, gifts, fees for golf, or any item, the purchase or possession of which is illegal. These restrictions could potentially impact a student or booster activity that makes gifts, grants scholarships or conducts a golf outing.

Key to the GASB 84 analysis is the fact that the prohibitions on expenditures under Section 1814 only apply to the expenditure of "public funds." Section 1814 does provide a definition of "public funds" as well as an important exception for "voluntary contributions made for a specific purpose." Below are the pertinent parts of Section 1814, including the exception under subsection (5):

"(1) Except as otherwise provided in subsection (2), a person shall not use school district,… funds or other public funds under the control of a school district,… for purchasing alcoholic beverages, jewelry, gifts, fees for golf, or any item the purchase or possession of which is illegal."

"(5) As used in this section, "public funds" means funds generated from taxes levied under this act, state appropriations of state or federal funds, or payments to a school district, … for services, but does not include voluntary contributions made for a specific purpose by a … board member; … employee; another individual; or a private entity." [Emphasis added]

We expect that most of the activity funds held by school districts which end up in the General or Special Revenue Fund should be able to meet the "voluntary contributions made for a specific purpose" exception under Section 1814 to the definition of "public funds." Although these funds may arise from fees, dues or fundraising activities, we believe they would be voluntary in nature and typically are being contributed in order to carry out the activity's purpose. Funds which are deemed to be voluntary contributions for a specific purpose would not be subject to the Section 1814 restrictions. Funds that fall under this exception could be expended for any expenditure as long as they have a reasonable educational nexus to the operation of the school district. Most of these activities should not have a problem meeting the educational nexus requirement due to the fact that they are for the benefit of the school and/or its students.

Scholarships for Post-Secondary Education

We also wanted to discuss the legal concern we have regarding activity funds and private purpose trust funds that offer scholarships to students for post-secondary education. We recommend that activity funds or trust funds that offer such scholarships should be set up so that they qualify as a fiduciary activity reported in the Fiduciary Fund or be moved to an entity or organization outside of the school district. If the activity fund or private purpose trust fund is required to be accounted for in the General or Special Revenue Fund as a governmental activity, these types of scholarships may not have a reasonable educational nexus to the operation of the school district, so as to be an allowable expenditure from the General or Special Revenue Fund.

Procurement/Purchasing Requirements?

The final legal concern which has been raised is whether state law and a school district's policies regarding the procurement of supplies, materials and equipment would be applicable to expenditures of funds for these student activities, clubs and booster groups that are now required to be reported in the General or Special Revenue Fund. Although there is an argument that these funds are not public funds or that the supplies, materials or equipment may not be owned by the school district, from a best practices standpoint, it would be in the best interest of these groups to apply these procurement laws and policies to these activities when the purchases meet the spending thresholds. The state law requirements and board policies are intended to safeguard these funds, and we believe that these safeguards would be beneficial to expenditures made on behalf of these student activities, clubs and boosters. Procurement policies and procedures may need to be updated to reflect the application of GASB 84 to purchases related to student activities, clubs and booster groups.

CONCLUSION

School districts should keep these legal considerations in mind during the GASB 84 implementation process. From a legal standpoint, activities that end up in the Fiduciary Fund will not be treated any differently than the prior Custodial Fund. We believe the two most common legal questions will arise with respect to the definition of "administrative involvement" when defining a fiduciary activity and "voluntary contribution for a specific purpose" when determining allowable expenditures from the General or Special Revenue Fund.

Hopefully, the implementation process will be a positive one which allows school districts to assess the various activity funds they currently maintain. As part of this process, school districts may determine that an activity should be maintained outside of the school district. Once the dust settles on the implementation of GASB 84, school districts should also review their Board policies to make sure that they reflect the school district's policies on its activity funds under GASB 84.

If you have any questions about the legal impact of GASB 84, please contact your Miller Canfield attorney or any of the authors listed on this alert.

[1] Governmental Accounting Standards Board ("GASB") Statement No. 84

[2] Bulletin 1022 – CHANGE NOTICE #29

[3] GASB Exposure Draft: Proposed Implementation Guide of the Governmental Accounting Board (December 17, 2018).

[4] In this example, GASB reasoned that the establishment of fees related to the generation of funds is analogous from a revenue standpoint to the example provided of determining eligible expenditures.

[5] See MCL § 380.11a.